Despite subdued growth by ‘anchor’ stores in shopping centres during the 2014-2015 financial year (FY15), the changing mix in centres is contributing to specialty shop outperformance, according to leading property and planning consultants, Urbis.

Traditional ‘anchor’ stores have been affected by ‘cannibalisation’ from new store openings, as well as intense price competition and low inflation.

During FY15, Coles, Woolworths and ALDI opened 82 new supermarkets around Australia. Kmart, Target and Big W also opened 24 new discount department stores. This level of new store openings in an otherwise low growth and low inflation market has resulted in supermarkets and discount department stores in shopping centres having a quiet year in terms of top line revenue growth.

In releasing the Urbis Shopping Centre Benchmarks 2015, Urbis Director of Economics and Market Research, Ian Shimmin, says that the strong performance of specialties, the continuing evolution of centres to include more non-retail uses, and the growth of mini-major stores (stores in excess of 400 sq.m) have clearly been the main themes affecting shopping centres this year.

“The stores typically referred to as ‘anchors’, because they have traditionally driven customer traffic flow in shopping centres, have stagnated. Compounding this trend is the fact that department stores, which have been the mainstay of the large regional centres, have grown by less than 0.5% overall,” Mr Shimmin said.

Despite this, shopping centres have continued to be important community focal points for a range of functions, not just shopping. They are broadening their mix of uses by including libraries, gyms, offices, personal and business services, as well as cinemas. Fine tuning the tenancy mix in centres to best suit the needs of the market, and to deal with change, are hallmarks of Australian shopping centre management.

In the larger centres in particular, the number of customers coming through has outstripped population growth, which clearly suggests that they are increasing in relevance. The tide continues to change and centres have continued to evolve, so much so that specialty stores (i.e. including those most affected by growth in online sales and competition from the majors) are adapting and winning.

“We’re seeing far more attention to shopfront design, visual merchandising and product differentiation in the better centres in Australia now, and consumers are responding positively,” Mr Shimmin said.

Regional shopping centres and CBD centres have been the standout asset classes in FY15, with specialty stores in these centres increasing by 4.3% and 4.4% respectively, on a like-for-like basis.

Mr Shimmin reports that across all shopping centre classes, specialty store growth has outstripped the growth recorded by the majors.

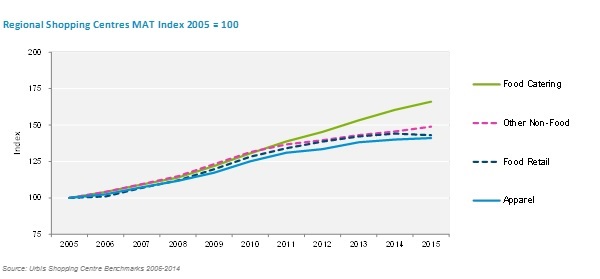

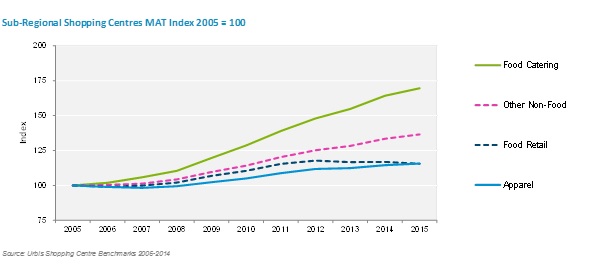

“This year, we’ve also seen specialty growth in some surprising categories. For example, books are making a comeback in regional centres, and music/video/games stores are one of the main growth categories in both regional and sub-regional centres. These are categories previously impacted by online sales,” Mr Shimmin said.