Locked down but not out: National Apartment Market on the improve in NSW, VIC; WA sales strong and QLD goes for gold.

5-second summary:

- Locked in by lockdown fuels buyers desire for more space, better amenity and stability.

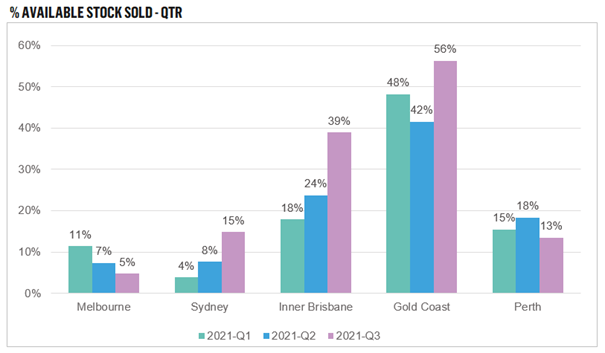

- Gold Coast apartment sales soar, clearing between 42-56% of available inventory each quarter of 2021.

- Brisbane pace of sales has almost doubled from levels being seen in 2020/21, since announcement of Brisbane 2032 Olympics.

- Melbourne sales slow, while Sydney’s high housing prices have placed more focus on the apartment market and seen the rate of sales at the highest level since 2017.

- Perth saw another solid quarter of sales as the market gears up from a strong summer of project launches.

Apartment sales: a Covid clearance

Nationally, the speed of sale of apartments illustrates that each city is operating in a different time zone when it comes to lifestyle, lockdowns and market activity. Markets weighed down by lockdowns will be buoyed by the encouraging results of those emerging and chasing the performance in states that have been able to operate with freedom and improving trading conditions.

Throughout 2021 Perth and the Gold Coast have continued to trade consistently and more strongly than in recent years with Perth projects selling an average of 16% of available inventory each quarter since the turn of the year. Sales in the Gold Coast have been flying with projects clearing anywhere between 42% to 56% of available inventory each quarter this year. The Gold Coast’s enviable lifestyle is a key driver for both local and interstate buyers.

Brisbane has continued to pick up the pace on sales, progressing from 18% earlier in the year to 39% of available inventory clearing in the quarter.

While Melbourne tipped back into power save mode for lockdown, clearing 5% of available inventory, the jump achieved in Sydney to 15% signals that reopening the economy, workplaces and real estate market can drive greater activity once again, as it had started to upon reopening last year.