On the face of it, build to rent in Australia has made great strides in the last 12 months, quickly transitioning from an overseas case study to over a billion dollars of planned projects across the country.

Softer sales conditions and a 26% drop in project launches in Q2 2018 year-on-year has focused the minds of land owners, government and developers. There is strong mutual interest in attracting counter-cyclical investment in housing and recognition that BTR can propel the pipeline at a time when build to sell is losing traction.

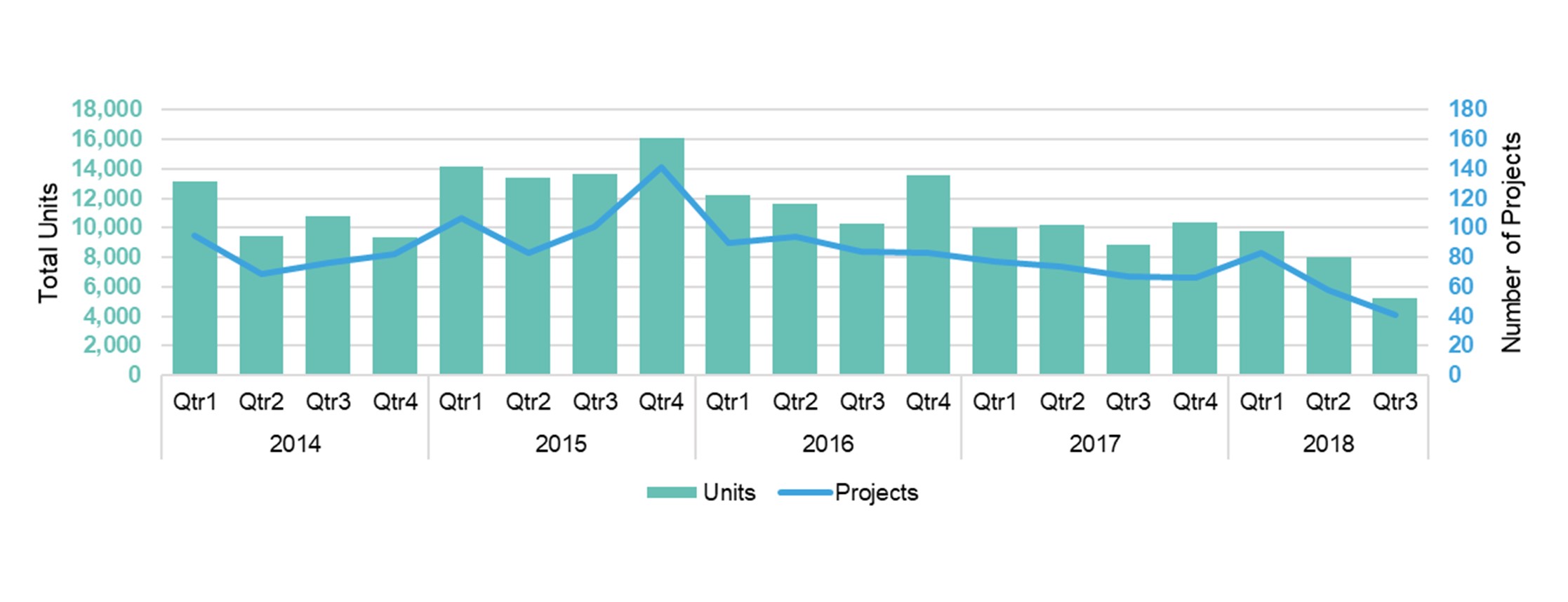

National historical & projected apartment launches

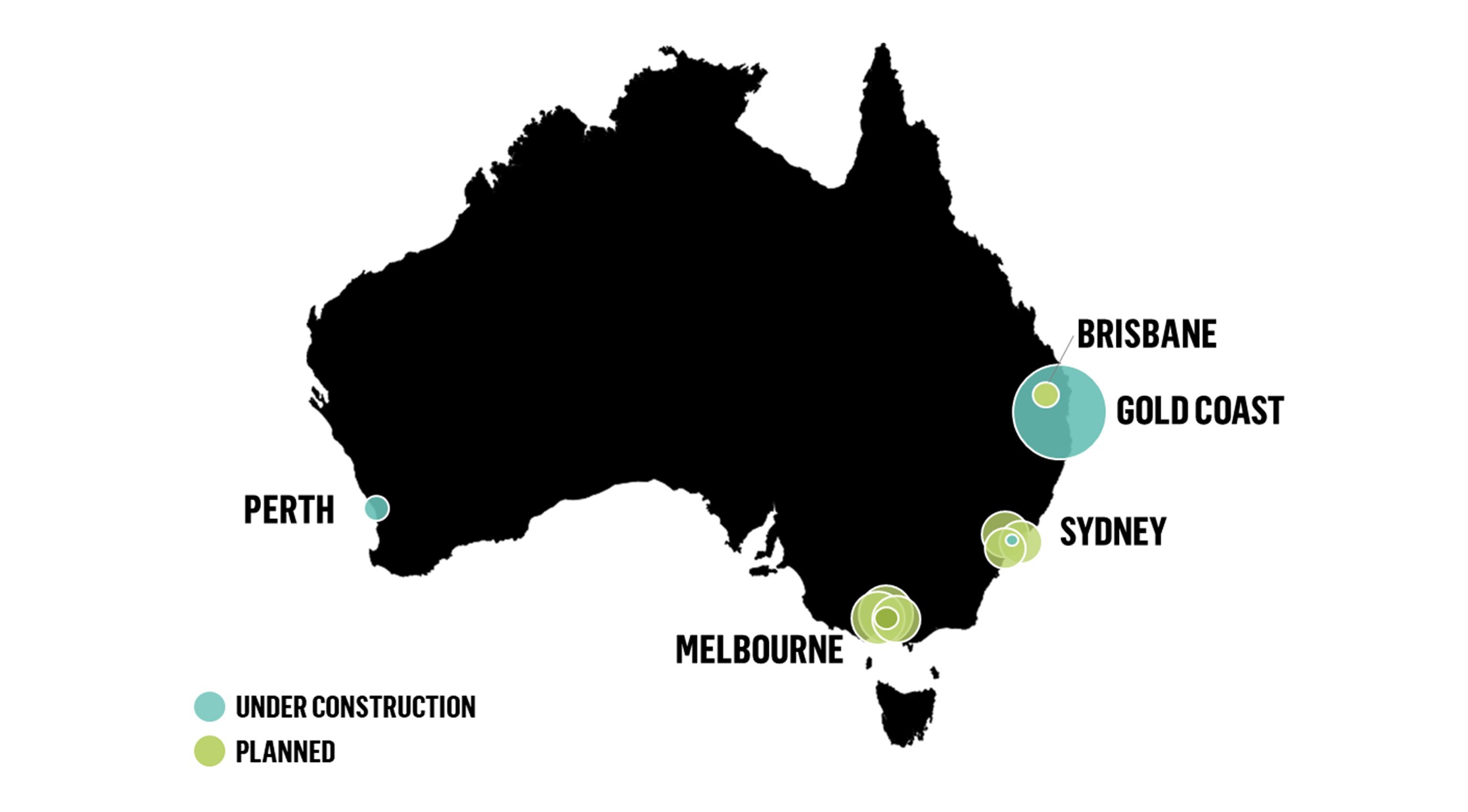

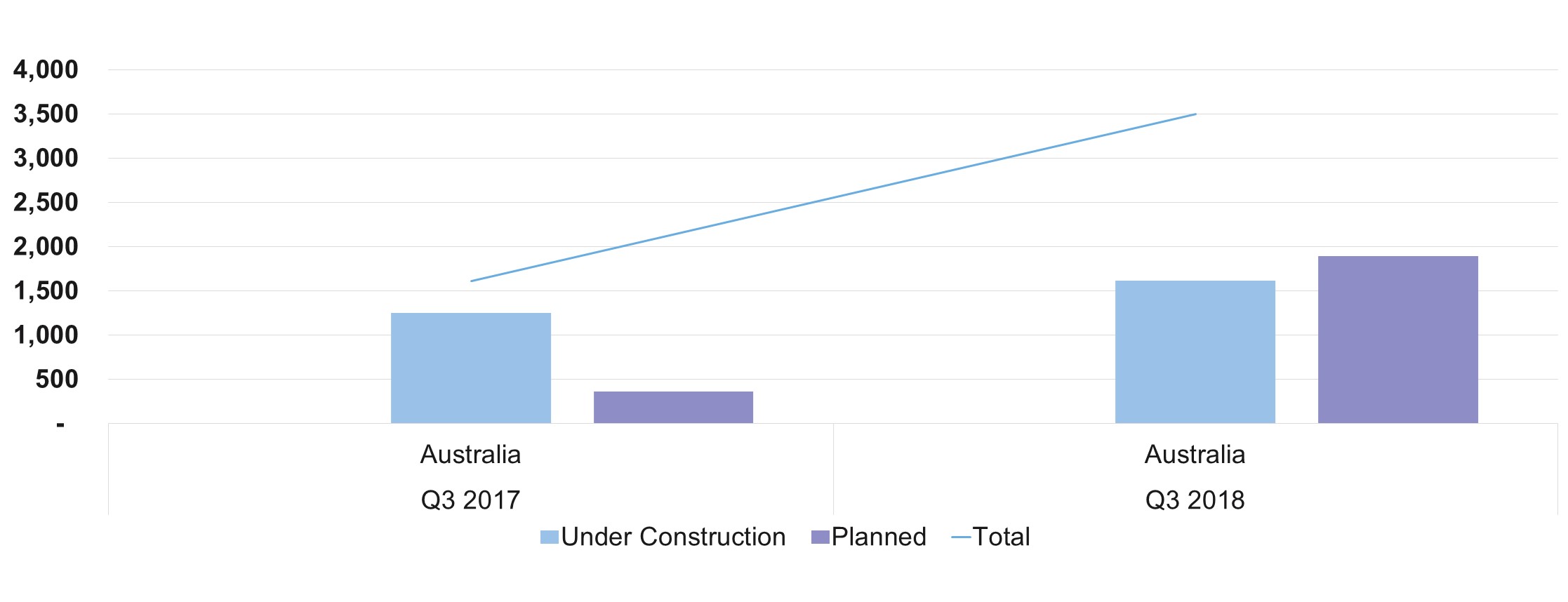

Urbis is tracking the build to rent pipeline closely, integrated with our Urbis Apartment Essentials reporting. Across Australia, there are around 3,500 BTR units in planning and development – up from 1,600 this time last year. It is likely many more existing permits will be revisited if the recent market trends continue, while more purpose designed BTR projects will emerge following proof of concept.

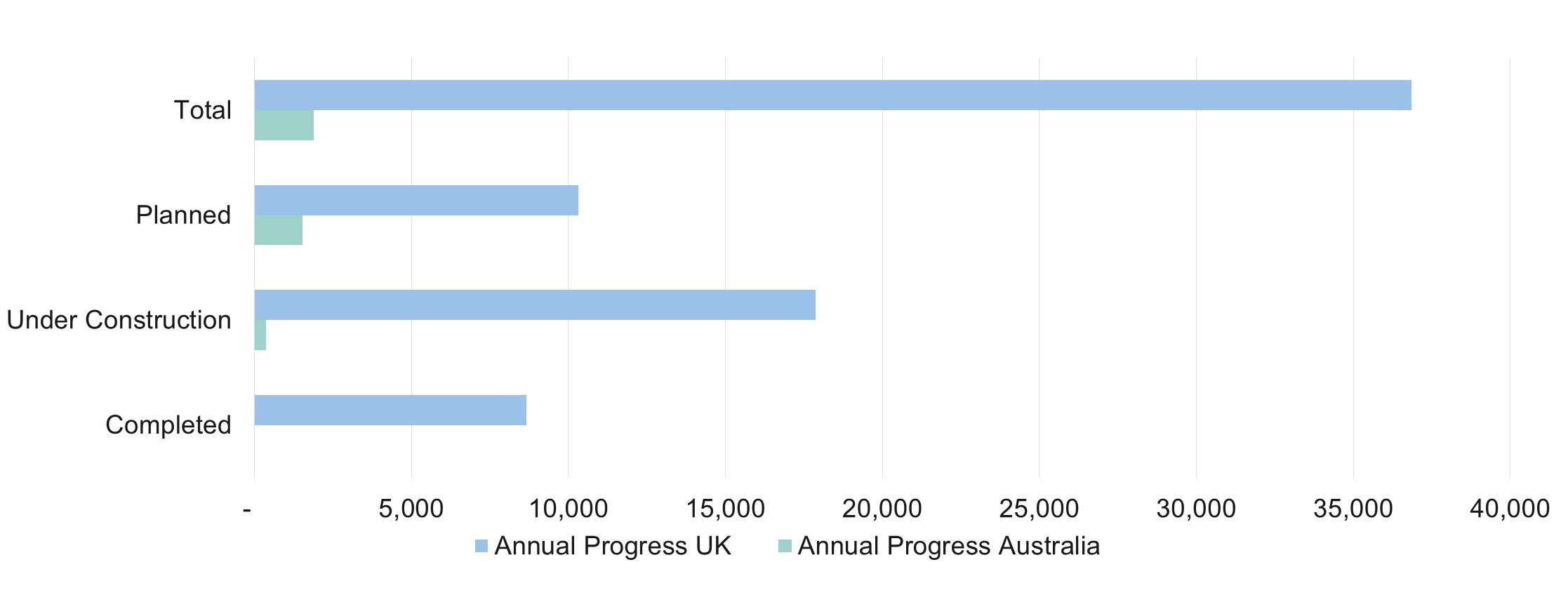

Tracking build to rent progress

As for market potential, a test run of over 9,000 entries in our new Urbis National Rental Tracker reveals there is a willingness to pay a premium for high quality new rental stock over the market median. In some inner-city BTR hot spots, customers are willing to pay 20% more for a new apartment with higher amenity.

Even markets that have been experiencing a surge in supply, are returning low levels of vacancy – with a sample of 30 new Brisbane apartment projects recording 98.7% occupancy, while rental growth has been outstripping price growth amid the changing dynamics across markets.

These trends lead us to believe there is appetite and room for a wider service offer in the rental market as the proportion of renters continues to increase and the profile of renters continues to diversify. Keeping track of these trends and mapping market dynamics will be key to building and managing a successful build to rent portfolio. Providing greater choice, service and diversity can ensure the benefit of additional supply flows through to Australians across the entire housing spectrum, from the most luxurious, to the most widely affordable.

A growing build to rent pipeline