Nationally, the apartment market has stabilised in Quarter 3 2019. This trend has been seen to benefit certain types of buyers capitalising on the markets current condition, taking their time to compare apartment options prior to purchase.

Urbis’ Apartment Essentials has been capturing and analysing the sales and supply data from five markets across the country since 2015. Following, we highlight Australia’s infrastructure investment opportunities and the potential red flags for the national apartment market.

Steady the ideal setting for owner-occupiers

The latest Urbis Apartment Essentials results for Quarter 3 2019 have reported steady sales with 9% of available stock selling, the same rate recorded in the previous quarter, as the market stabilises.

“Residential apartment market activity has remained below the peak witnessed in 2015/2016 across the national market, and given fewer new apartment project launches, it is unlikely that we will be witnessing this level of activity again over the next 12 months,” Mr Clinton Ostwald, Group Director at Urbis said.

“However, when looking at the market holistically the slower but stable market is a good setting, as it is making room for owner-occupiers who feel they have more opportunity than at the peak when investors dominated.”

If the price is right

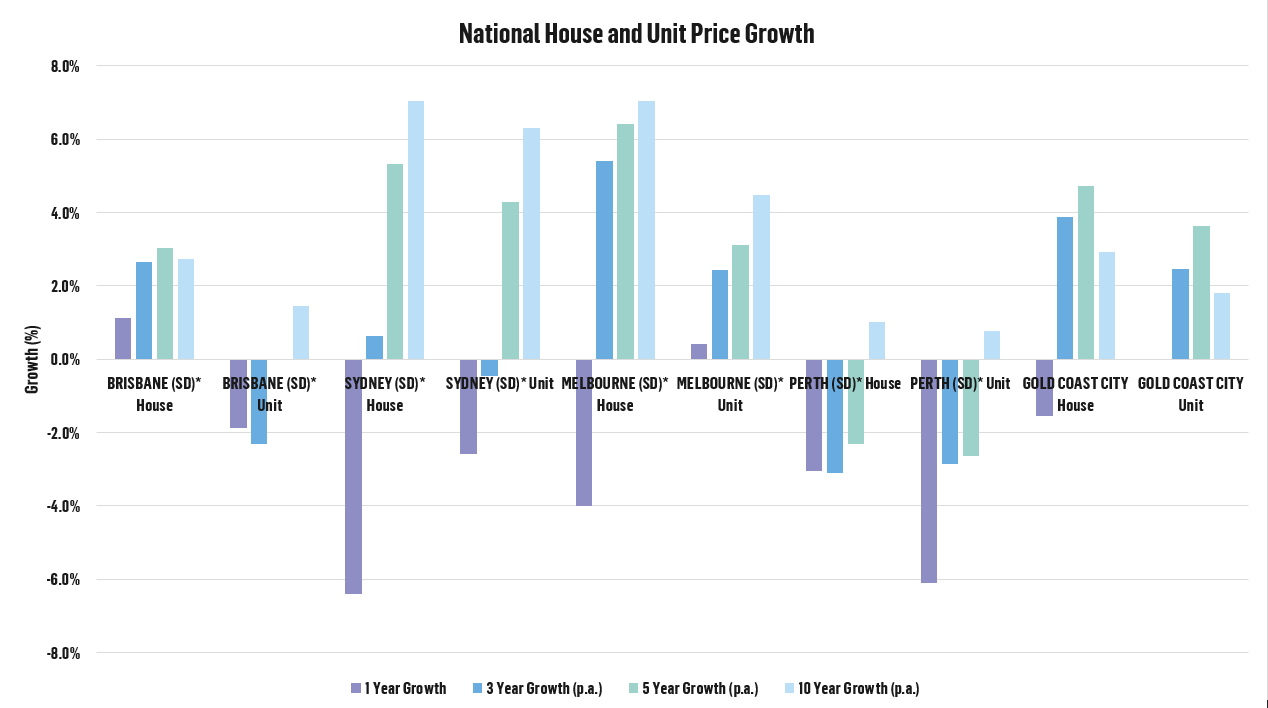

Record low interest rates are expected to spur on house price growth across the national markets, with gains already witnessed in Sydney and Melbourne. Urbis’ Apartment Essentials monitoring of new apartment sales has registered limited price growth across new apartments, with prices remaining relatively stable over the past quarter.

Over the past three years the Urbis Apartment Essentials data shows limited changes in price across the five cities, especially when looking at the core selling one-bedroom, one-bathroom and two-bedroom, two-bathroom product. However, no significant price drops can be seen, with new apartments holding their value.

Pricefinder reports that with the exception of Perth, established unit prices have ranged from -2.6% loss in Sydney to 0.4% growth in Melbourne in the past 12 months.

“Though Sydney units recorded a small decline in value they fared well when compared to houses. which recorded a -6.4% fall in price over the past 12 months,” Mr Ostwald said. “Property is a long term investment, and looking back five years both houses and units have still recorded overall growth in the Sydney, Melbourne, Brisbane and Gold Coast markets despite recent declines.”

National House and Unit Price Growth. Source Pricefinder. Click to enlarge.

Clearance Rates

Auction clearance rates across the country have lifted, especially in Sydney and Melbourne, further pointing to a turnaround for the residential market. Corelogic reports recent auction clearance rates of between 70% and 80% for Sydney and Melbourne, and between 20% and 50% for Perth and Brisbane. One year ago, Melbourne and Sydney were sitting at around 50%, Brisbane at 40% and Perth 11%.

“The great Australian dream of home ownership is still alive, and current market conditions are helping to make that dream come true” Mr Ostwald said.

“Our Apartment Essentials research points towards owner occupiers making up the majority of purchases across all cities except for the Gold Coast, where Interstate Investors have the majority share. Though the dream of home ownership may not have changed, a home is no longer necessarily a house with a backyard, with many choosing apartments for price, location and ease of lifestyle.”

Q3 2019 Apartment Essentials Snapshot

9% of the surveyed available stock was sold in the September quarter across the five markets, with no change from the previous quarter:

Sydney (8% of available surveyed stock sold, 1,325 new apartments launched)

Melbourne (10% of available surveyed stock sold, 1,687 new apartments launched)

Brisbane (10% of available surveyed stock sold, 89 new apartments launched)

Perth (7% of available surveyed stock sold, 155 new apartments launched)

Gold Coast (8% of available surveyed stock sold, 195 new apartments launched)

National weighted average sale price recorded at $705,452 for Q3 2019

Sydney – $930,035

Melbourne – $620,707

Brisbane – $748,829

Perth – $638,830

Gold Coast – $741,878

The most popular product type was two-bedroom, two-bathroom product at 47% of total sales. Across the cities the highest selling product types were:

Sydney – Two-bedroom, two-bathroom apartments – 51%