Some reports suggest we are at a crisis point in terms of rental affordability. Other reports suggest that the market is oversupplied with apartment and rental stock. I suggest we are just finding our balance following a tumultuous couple of years under the cloud of Covid.

Melbourne’s Rental Markets

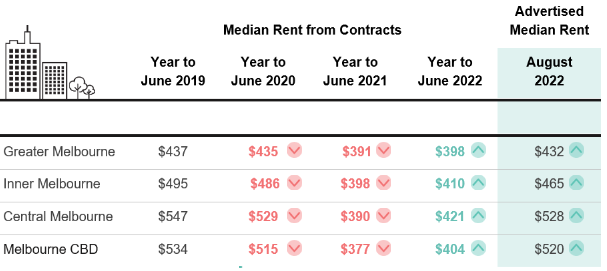

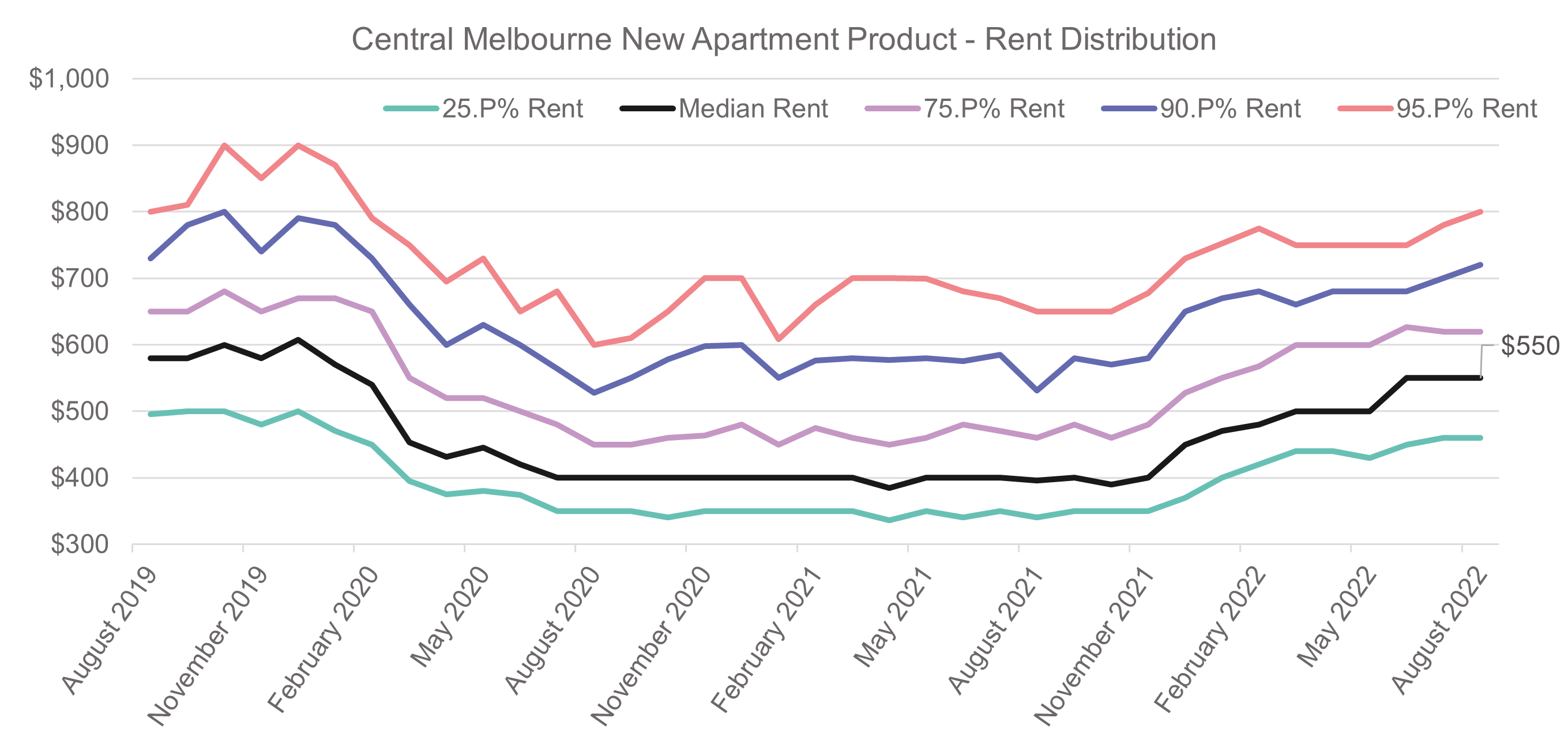

Let’s look at Melbourne – the city that was most impacted by Covid induced lockdowns and the impact this had on the various residential rental markets across the city. This is important perspective to help understand what has happened in the market over recent months and that the residential market is made up of many micro-markets.